-

AuthorPosts

-

-

Economic Divide and

Growth Potential:

Analyzing Africa’s

Top Five Economies

and the Path

Forward.

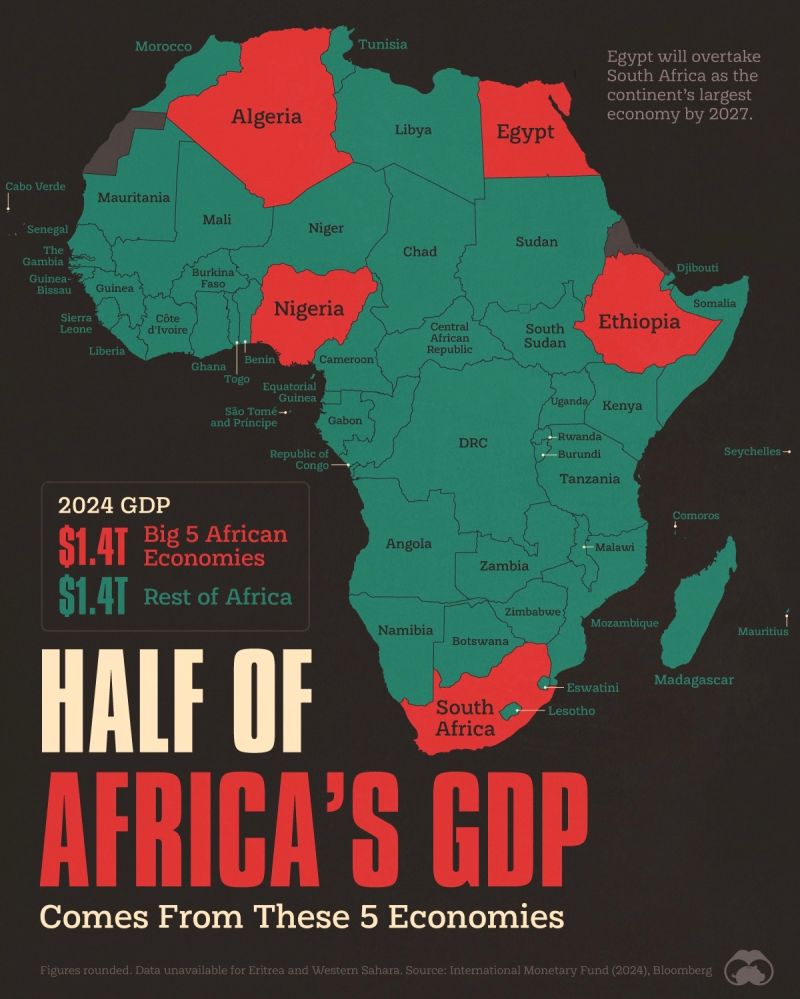

Abstract: Africa’s economic landscape is defined by a marked divide between its leading economies and the rest of the continent. Five countries—South Africa, Egypt, Algeria, Nigeria, and Ethiopia—account for half of Africa’s Gross Domestic Product (GDP), reflecting both the challenges and opportunities facing the continent. With a combined GDP of $1.4 trillion, these nations dominate the economic output of a continent made up of 54 countries, where the remaining nations share an equal amount of GDP. This article examines the underlying reasons for this economic divide, explores the growth potential within Africa, and discusses strategies to foster inclusive economic development, particularly through frameworks like the African Continental Free Trade Area (AfCFTA) and targeted investment in local value chains.

Introduction: In 2025, Africa stands at a pivotal moment in its economic trajectory. With half of its GDP stemming from just five countries—South Africa, Egypt, Algeria, Nigeria, and Ethiopia—the continent exhibits a stark economic divide. This imbalance highlights both challenges in creating sustainable, widespread economic development and the untapped potential of many African nations. As Africa continues to grow, with a projected increase in consumer spending of over $3 trillion by 2030, the question arises: can the continent bridge the economic gap and ensure that its growth benefits all of its citizens?

The Economic Divide in Africa: The economic disparity in Africa is stark. South Africa, the largest African economy by GDP, leads the pack with a GDP of $373.23 billion, followed by Egypt ($347.59 billion), Algeria ($266.78 billion), Nigeria ($252.74 billion), and Ethiopia ($205.13 billion). Together, these countries represent half of Africa’s total GDP, which stands at approximately $2.8 trillion. The other 48 nations—accounting for the majority of the continent’s population—share an equivalent GDP, underscoring the uneven economic development across the region.

This disparity reflects the historical and structural factors that have shaped African economies, including colonial legacies, political instability, and inconsistent access to resources. While the top five economies benefit from stronger industrial bases, better infrastructure, and more significant foreign direct investment (FDI), many other African countries face challenges such as limited access to capital, a lack of skilled labor, and weaker governance frameworks.

Africa’s Economic Potential: Despite the challenges, Africa has significant economic potential. Over the past decade, some African countries, cities, and companies have emerged as beacons of innovation, productivity, and growth. Notably, nations like Kenya, Ghana, and Côte d’Ivoire have demonstrated resilience and growth, offering models for other regions to follow. These successes indicate that with the right investments and strategies, African economies can break out of the patterns of stagnation that have historically limited their growth.

Africa’s growing population, currently estimated at over 1.4 billion, is projected to reach 2.5 billion by 2050. This demographic shift presents a unique opportunity: with rising incomes and a growing middle class, African countries can unlock significant consumer spending. By 2030, it is estimated that 250 million Africans will join the consuming class, creating a $3 trillion market. This presents both challenges and opportunities for businesses seeking to scale their operations and innovate within local value chains.

The Role of the African Continental Free Trade Area (AfCFTA): One of the most promising initiatives for addressing Africa’s economic divide is the African Continental Free Trade Area (AfCFTA). As of now, all 12 of the continent’s largest economies, including South Africa, Egypt, Algeria, and Nigeria, are members of AfCFTA, a framework designed to facilitate intra-African trade by eliminating tariffs, reducing trade barriers, and harmonizing regulatory standards. AfCFTA has the potential to unlock economic growth across the continent by promoting trade between African nations, improving access to markets, and creating a unified economic space.

AfCFTA’s goals go beyond simple tariff reduction. By facilitating smoother movement of goods, services, and capital, it aims to stimulate industrialization, encourage the growth of small and medium-sized enterprises (SMEs), and diversify African economies away from their traditional reliance on raw material exports. The effective implementation of AfCFTA can also foster economic resilience, reduce dependency on external markets, and encourage regional collaboration on infrastructure projects, such as the Trans-African Highway.

Unlocking Africa’s Growth Potential: For Africa to achieve sustainable and inclusive growth, several key factors need to be addressed:

Investment in Infrastructure: Africa’s infrastructure deficit remains a significant challenge to economic growth. Improved transportation, energy, and digital infrastructure are essential for enabling intra-Africa trade and supporting business development. The AfCFTA and the African Development Bank (AfDB) are working on initiatives to address these gaps.

Education and Skill Development: To foster innovation and industrialization, African countries must invest in education and skill development. A well-trained workforce is critical for supporting technological advancements and improving productivity.

Support for SMEs and Local Enterprises: SMEs play a crucial role in driving economic growth in many African nations. Supporting these businesses with access to finance, technology, and training will enable them to contribute more significantly to local economies and the broader African market.

Promoting Innovation and Entrepreneurship: African nations must continue to support innovation ecosystems that foster entrepreneurship. Initiatives such as Africa’s “Silicon Savannah” in Kenya and Nigeria’s tech hubs are proving that the continent has the potential to become a global leader in technology and innovation.

Diversifying Economies: Many African economies are heavily reliant on natural resources. Diversifying these economies into manufacturing, services, and technology sectors will reduce volatility and create more stable, sustainable growth.

Conclusion: The economic divide in Africa, while significant, is not insurmountable. By capitalizing on the continent’s vast potential for growth—driven by a young, dynamic population, increasing urbanization, and rising incomes—Africa can achieve a more equitable and prosperous future. Initiatives like the African Continental Free Trade Area (AfCFTA) provide a framework for accelerating intra-Africa trade, improving infrastructure, and creating a more unified market.

As the continent works towards achieving the goals of Agenda 2063 and the African Union’s vision for economic integration, the focus must be on inclusive development. Bridging the economic divide, investing in human capital, supporting local enterprises, and fostering innovation will unlock the full potential of Africa, transforming it into a global economic powerhouse.

Keywords: Africa, GDP, economic divide, AfCFTA, economic growth, infrastructure, SMEs, innovation, investment, Agenda 2063, trade, consumer spending, entrepreneurship.

References:

- African Union. (2023). Agenda 2063: The Africa We Want. African Union Commission.

- African Development Bank. (2022). AfDB Annual Report: Africa’s Infrastructure Needs. African Development Bank.

- World Bank. (2023). Africa’s Economic Outlook. World Bank Group.

- United Nations Economic Commission for Africa. (2021). Economic Report on Africa 2021. UNECA.

-

-

AuthorPosts

You must be logged in to reply to this topic.